Articles

The great gas investment divide

There is a developing consensus in the debate on how humankind should approach decarbonising energy supplies to avert dangerous climate change about the appropriate roles for most major primary energy sources.

For example, a phase-out of coal—as the most carbon-intensive of fuels—garners widespread agreement, and the list of countries that have committed to this goal grows by the month. Conversely, renewables such as wind and solar power are viewed increasingly positively because they emit no greenhouse gases (GHGs) during operation and their costs continue to fall.

Gas stands out as an exception to this general rule, dividing experts, making life uncomfortable for investors, and threatening progress towards Paris Agreement targets. “I have built models of how we can decarbonise the world twice over,” Rob West, principal research analyst at energy technology consultancy Thunder Said Energy told the Petroleum Economist LNG-to-Power Emea forum in early November. “And the lowest-cost way I can get to net-zero [carbon] energy by 2050 is to treble the demand for natural gas. We are going to have 400tn ft³ [11.32tcm] of gas in this energy system.”

West believes that growing populations and rising energy use in the developing world will boost global demand for energy from 70,000TWh/yr today to 120,000TWh/yr by 2050. “The reason that number matters,” he says, “is because wind and solar are currently growing at a combined rate of about 300TWh/yr. But it has got to build into a 120,000TWh/yr energy system—and so we are going to need other fuels. Gas meets a lot of that need in our models.”

Chemistry

At the heart of West’s argument is the chemistry of the main component of natural gas, methane, which consists of one atom of carbon and four of hydrogen. This high hydrogen content not only means that gas emits much less CO2 than coal when burned, it also makes gas an ideal feedstock for production of so-called ‘blue’ hydrogen through reforming.

“The lowest-cost way I can get to net-zero [carbon] energy by 2050 is to treble the demand for natural gas” West, Thunder Said Energy

“One of the largest sources of growth for gas is creating blue hydrogen,” says West. “Green hydrogen [produced by the electrolysis of water using power from renewables] is a bubble; the economics do not come anywhere close to working and they never will. Blue hydrogen is going to be able to deliver large amounts of usable heat and power at about $1.45/kg.”

West is concerned that “a lot of people just are not looking at the numbers”, with the consequence that there may not be enough gas to go around.

But what happens in his vision to the methane’s carbon atoms? The answer is twofold: firstly, a major push to develop carbon capture and storage (CCS), not least because the technology is needed for production of blue hydrogen; and, secondly, “nature-based solutions” such as the planting of trees, because, he adds, “the single largest source of CO2 emissions on the planet is deforestation”.

“I have done some detailed models around CCS, and it is all about scale,” says West. “You can get a CCS value chain to work at about $70/t CO2e. However, this is for a multi-million t/yr CO2 disposal facility, taking CO2 out of a high-concentration, 50-60pc, exhaust stream.

“If you build a big blue hydrogen plant, you take that CH4 molecule, you split it into CO2 and H2 at a giant multi-million t/yr plant. All of the carbon goes straight into a big pipe, into a big disposal facility. And the hydrogen can go and decarbonise lots of other stuff.”

Abatement

Unlike West, Christof Ruehl—senior research scholar at Columbia University’s Center on Global Energy Policy and a former BP group chief economist—is more sceptical about humankind’s ability to simultaneously meet growing energy demand while mitigating climate change.

120,000TWh/yr – Global demand for energy by 2050

“It is very unlikely—impossible almost—that we will get anywhere close to the Paris targets,” he says. “If you want to support economic growth, you will have GHG emissions which will make the Paris targets impossible to reach. It is time for a dose of realism.”

He is also sceptical about the role of CCS, which he sees as “clumsy, expensive and making sense only where you produce oil and gas”. “When I look at the scale of the problem, most of us are still talking too much about abatement, about how to prevent releasing GHGs into the atmosphere,” says Ruehl.

“That is not going to do the trick. So we will also have to talk about how we get it out of the atmosphere. We will not get it out of the atmosphere with CCS. To help us get anywhere close with Paris targets we will need to have offsets.”

Designing a system that is not vulnerable to fraud will be tough, he says, pointing to problems that have arisen in the past with the EU’s emissions trading system–and calling on lawyers, economists and industry to work out an effective regulatory framework with appropriate governance.

Shale rush

Ruehl is also bullish on longer-term gas demand, which, unlike coal and oil, he does not see peaking this side of 2050. He expects China to be a major driver, but to temper its import thirst through greater exploitation than thus far achieved of “the biggest proved shale gas reserves in the world”.

“[Barriers to producing shale gas] can be fixed and have always been fixed in the history of this industry. [In China], it is a matter of poor regulation and the wrong incentives and the wrong development model. The old centrally planned model will not get them there. China being China, they will correct it eventually.”

But potential investors in gas may, in Ruehl’s view, face future challenges for two reasons: growing awareness of unwanted emissions of methane, a potent greenhouse gas that will have to be controlled; and the push towards renewables as the energy transition gathers momentum.

“If you want to support economic growth, you will have GHG emissions which will make the Paris targets impossible to reach. It is time for a dose of realism” Ruehl, Center on Global Energy Policy

Ruehl remains sceptical that the Covid-19 pandemic will accelerate green development, because of its depressive impact on the prices of fossil fuels and also because societies will have less money to invest in still relatively expensive renewables. But he accepts that the impacts will vary from region to region.

The latest Energy Transition Outlook report from consultancy DNV GL projects that global gas use will continue rising until the mid-2030s, at which point it will peak and begin to decline.

But Bent Erik Bakken, senior principal scientist at the firm’s Energy Transition Programme and responsible for the models behind its Outlook model, agrees that there will be long-term demand for gas in blue hydrogen production and as a generation fuel to balance variable renewables. He is also bullish about the prospects for CCS, but not until after 2030

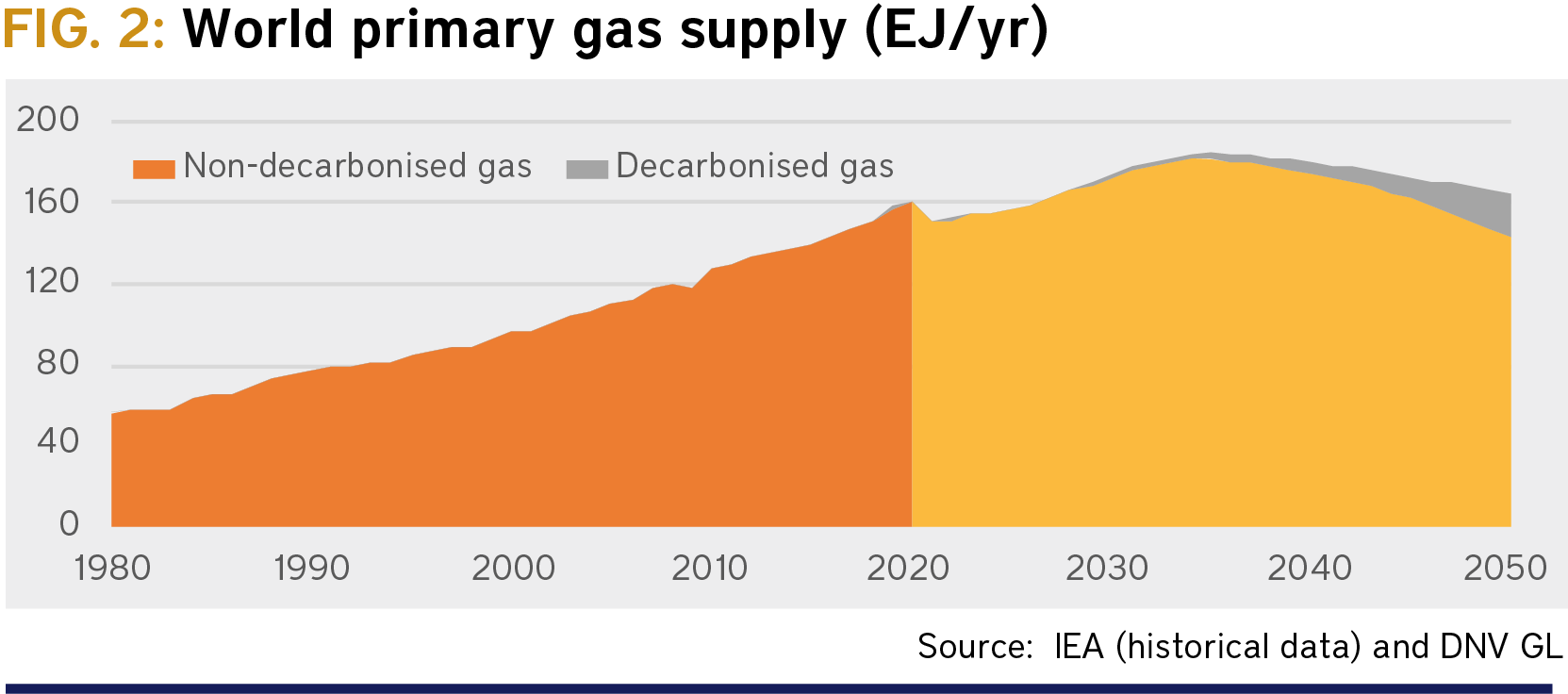

As for decarbonised gas, the DNV GL forecast projects that only 13pc of gas demand by 2050 will be met in this way, from the growth of blue hydrogen from methane reforming and gas with CCS in power and industry.

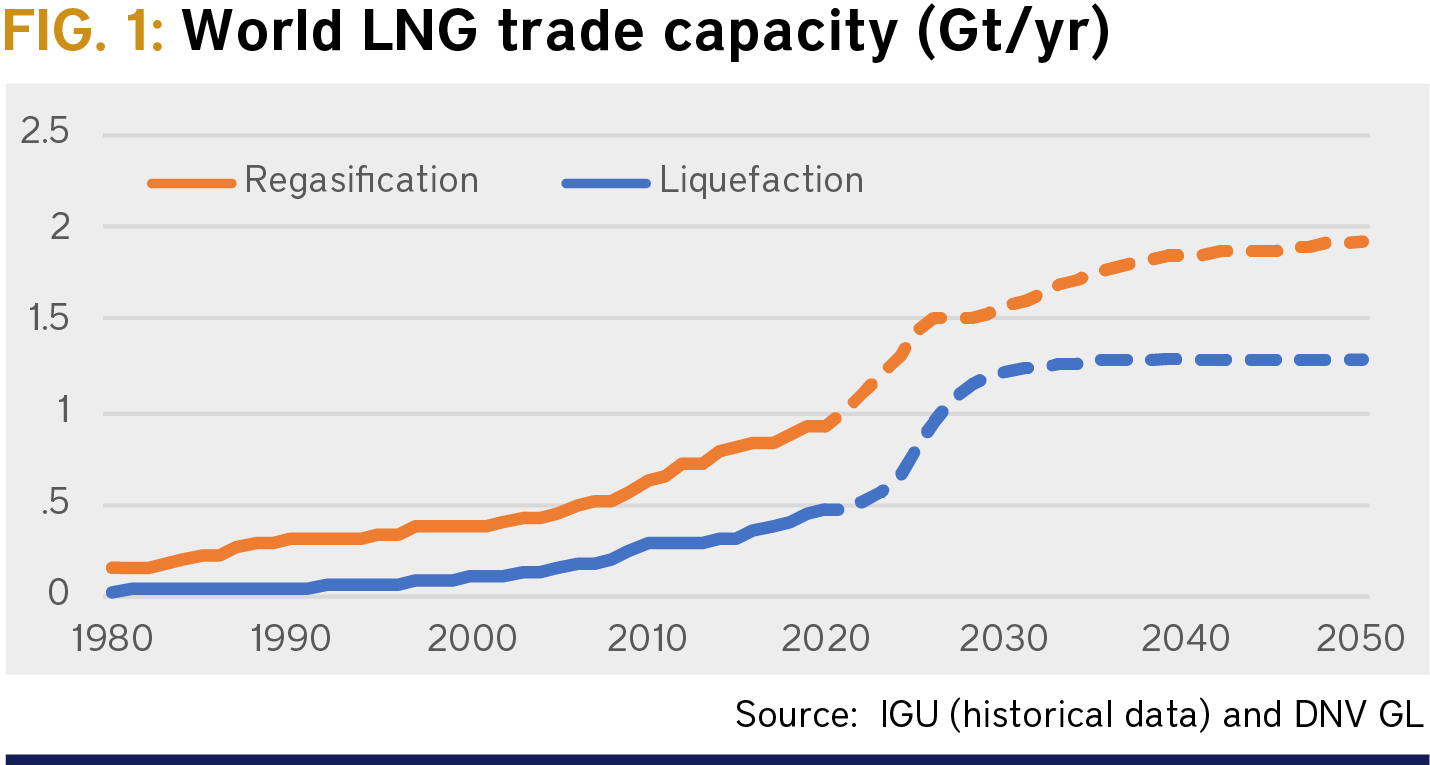

“In general,” says Bakken, “we see a lesser role for gas in 2050 than today.” But, to put that in context, DNV GL still projects that gas will be the world’s largest source of primary energy in 2050. And this will require rapid growth in LNG liquefaction and regasification capacity, with North America accounting for 44pc of global liquefaction capacity by 2050.

Petroleum Economist's second virtual LNG to Power Forum took place earlier this month with a focus on the opportunities and challenges for LNG across the Emea region. This virtual event included eight hours of high-quality content, with a focus on engaging and interactive live panel discussions. Content is now available on demand. Click here to view.

The first event in this series, LNG to Power Forum Apac, can be viewed here. The North America edition took place in December 2020, and can be viewed here.

Author: Alex Forbes

Related Articles

Connect with H2Tech